Searching for methods to ease retailers’ £25bn enterprise charges burden

We hear you. The message from politicians to retailers is that they understand that business rates are placing a disproportionate burden on an industry that had already undergone profound structural change before the pandemic.

Many of these politicians represent constituencies where the state of main streets, eroded by store closures and bankruptcies, is a defining issue for local voters.

The coronavirus pandemic has accelerated an existing shift to online shopping, driving chains like Debenhams and Arcadia into bankruptcy, losing hundreds of stores and tens of thousands of jobs.

“Things have changed since Covid,” said Jerry Schurder, Head of Business Rates at real estate consultancy Gerald Eve. “There is greater acceptance that business rates are simply no longer sustainable.”

According to Altus Group, another consulting firm, prices for more than 12,000 stores were higher than rent even before the pandemic began.

While retailers are currently exempt from tax under a year-long vacation that is extended by three months in the budget, ministers also like the £ 25 billion the tax normally collects each year in England alone – a quarter of that comes from Retailers. As with all property-related taxes, prices are easy to collect and difficult to avoid.

The interest rate cut was a conservative manifesto in 2019, and finding a way to do it without blowing a hole in tax revenue is the target of a Treasury Department review announced in April and due to deliver its conclusions this fall .

The Treasury Department has stated that it is ready to go beyond simply optimizing the administrative process. But it was also clear that any reduction would have to be offset by alternative sources of tax revenue.

The preferred option is an online sales tax of around 2 percent, an idea that is very divided.

More than a dozen retailers, including Tesco and Waterstones, recently signed a letter calling for an online sales tax to fund an interest rate cut.

But other executives and analysts oppose it. “I’m not in favor of it, and I don’t really understand the argument for it,” said Stuart Adam of the Institute for Fiscal Studies, a think tank.

He argues that such a tax would be passed on to consumers, while the benefit of lowering tax rates would largely be converted into rents – which would benefit landlords rather than retailers.

Alex Baldock, managing director of Dixons Carphone, recently said it would be both difficult to manage and to increase the tax burden.

Financial Times calculations suggest that Dixons and some other retailers could do even worse if an online sales tax were used to offset a drop in business rates.

Steve Rowe, executive director of Marks and Spencer, wrote in the FT that such a tax risks “stifling the innovation on which the future of the sector depends” and preventing companies like his company from using the e- Commerce to compete.

Business rates are based on market rental values as assessed by the Valuation Office Agency, part of HM Revenue & Customs. Baldock’s preferred method of lowering prices is through more frequent revaluations.

The last revaluation was in 2017, based on rents in 2015. Since then, shop rents have fallen sharply, while those for the huge warehouses used by Amazon and others have increased.

More frequent revaluation would accelerate the trend towards stores at lower rates and sheds at higher rates.

Lord Simon Wolfson, a conservative peer and executive director of the fashion chain Next, has argued that a similar result could be achieved if a different multiplier was applied to stock.

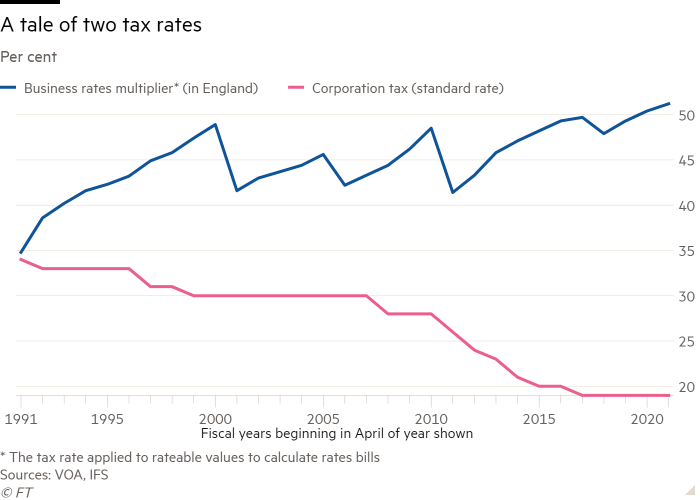

The multiplier is the tax rate that is applied to all assessable values in order to calculate the invoices. In England it has risen from 34.8 percent in 1990 to 51.2 percent today.

The consultation of the Ministry of Finance also brings this option to a standstill. Given that the next reassessment won’t happen until 2023, it would be the quickest, easiest way to fix the perceived imbalance between the rates retailers pay in-store versus their online-only counterparts. It would also retain the benefits of property-based taxation.

But it would remove the consistency inherent in the current system and open the door for continued lobbying by the industry to argue that they should pay a lower rate.

Many retailers believe that the long-term solution is a broader corporate tax reform. Rowe advocates a “modest” increase in the UK corporate tax rate – currently 19 percent – to offset a reduction in the multiplier to 35 percent.

However, others have privately voiced the view that while the standard corporate tax rate is set to rise to 25 percent in 2023, it is unrealistic to expect the additional revenue to be used to lower corporate tax rates once government debt reaches levels that seldom found outside the world is wars.

A final option is to replace the commercial tariffs with a property or capital value tax that is payable by the owner of the property, not the tenant. Adam said it would be a fairer, more efficient, and more economical thing to do in the long run for redeveloping real estate for other uses.

Regardless of the revenue-increasing alternatives, there are two other measures that go beyond lower multipliers and more frequent revaluations and could reduce the burden on corporate rates.

Recommended

One is to end the so-called transitional relief. This mechanism aims to alleviate the pain of a sharp spike in interest bills. However, because business rates must be revenue neutral by law, the increase in attenuation for some is paid for by limiting decreases for others.

Altus Group, a consulting firm, highlights a Poundland business in Blackpool, whose share in value was down 46 percent when it was last revalued in 2017. The aggregate rate bill for the next three tax years should have dropped to £ 175,644 – but transitional relief meant it actually paid more than £ 300,000.

The other measure would be to abandon the tax neutrality requirement for revaluations. At present, any decrease in the total assessable value is offset by a corresponding increase in the multiplier.

This ensures that government revenues remain constant, but it means that many businesses are seeing less passage due to falling rents.